Uncertainty Is Up—So Why Are Community Bankers Still Optimistic?

By CSBS Chief Economist Thomas F. Siems, Ph.D.

Economic uncertainty remains elevated, driven by geopolitical tensions, persistent inflation pressures, and a slowing labor market. Yet the latest CSBS Community Bank Sentiment Index (CBSI) points to a more nuanced reality. Although the overall index edged down slightly to 131 and uncertainty has increased—particularly around monetary policy—community bankers continue to express optimism about the year ahead. That resilience is notable given the increasingly complex backdrop facing policymakers, where higher oil prices tied to the war in Iran and sluggish job growth are complicating the Federal Reserve’s path toward price stability and maximum employment. Even so, confidence at the local level remains far more durable than national narratives might suggest.

Steady Optimism Despite Rising Uncertainty

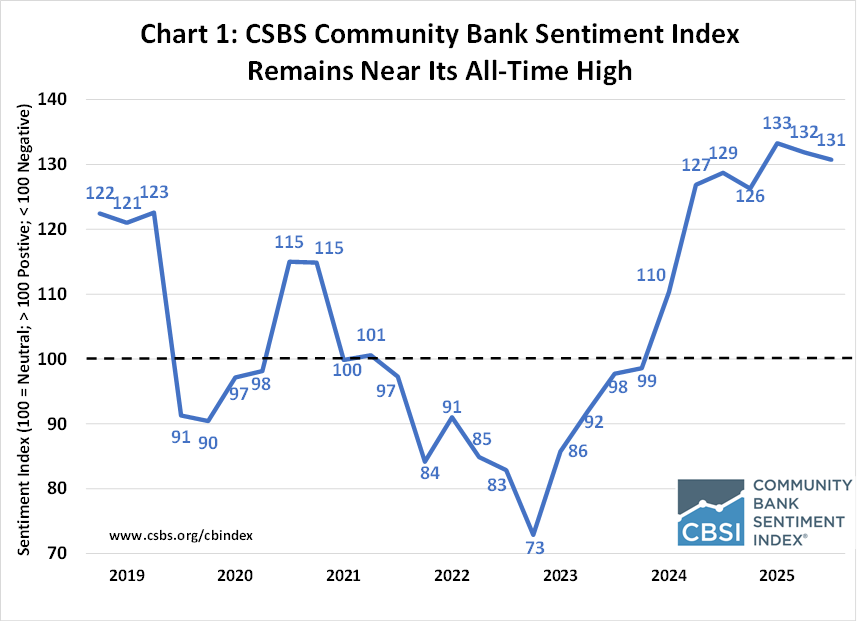

As shown in Chart 1, the CBSI has remained remarkably stable and elevated over the past year and a half, fluctuating within a narrow range of 126 to 133 and staying well above the neutral level of 100. Compared to one year ago, the index is up two points, continuing to signal strong positive sentiment. And since then, six of the seven components that make up the index have remained above 100; only the business conditions indicator has consistently been below neutral.

Policy Uncertainty Is Driving the Shift in Sentiment

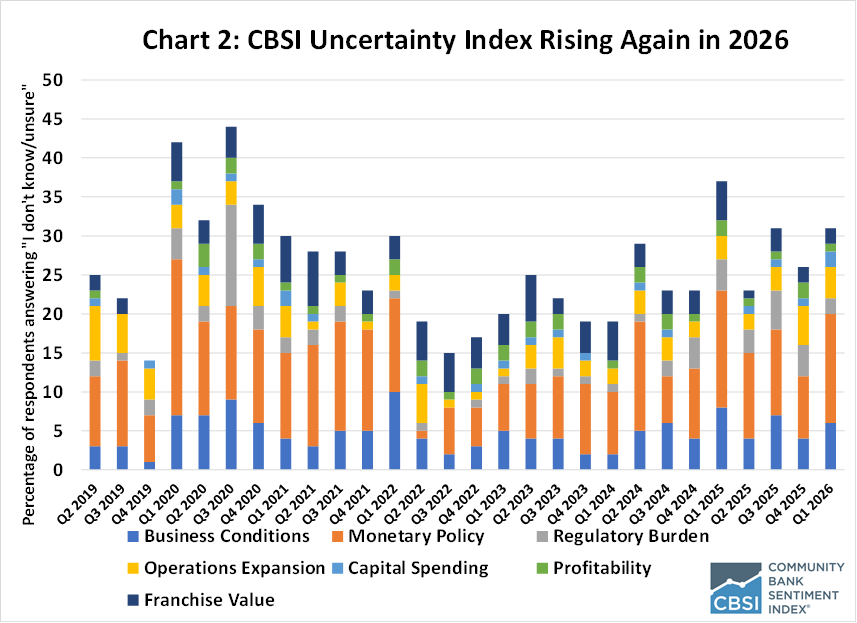

At 98, expectations for future business conditions declined one point from the previous quarter, while the metric to capture “uncertainty” increased more noticeably. The CBSI uncertainty index—calculated as the share of “I don’t know/unsure” responses across all seven components—rose five points to 31, the seventh-highest reading since the index began in early 2019. Open-ended responses suggest that much of this increase reflects growing concern about the national economic outlook, particularly in light of the war in Iran. Higher oil prices are adding to inflationary pressures and further complicating the Federal Reserve’s policy decisions.

The slight decline in the overall CBSI was driven primarily by weaker sentiment around monetary policy and regulatory burden, which fell by 13 points and 8 points, respectively. Offsetting these declines were gains in key performance indicators. The profitability index increased by seven points, while the franchise value indicator rose by two points to a new record high of 170, underscoring continued confidence in longer-term prospects.

Additional insight from the CBSI dashboard highlights how expectations shape overall sentiment. Among respondents, 18% expect business conditions to improve over the next year, 56% think conditions will remain unchanged, and 20% anticipate deterioration. These expectations strongly correlate with overall sentiment: banks expecting worsening conditions report a CBSI score of 96—below neutral—while those expecting improvement report a much higher score of 159. For the more pessimistic group, concerns about profitability and monetary policy are the primary factors dragging down sentiment.

Chart 2 further illustrates the rise in uncertainty, particularly regarding monetary policy. In the first quarter, uncertainty about the future impact of monetary policy accounted for 45% of total uncertainty, up from 31% at the end of 2025, making it the largest contributor to overall uncertainty.

This heightened uncertainty is also reflected in the Federal Reserve’s own assessment. In its March 18, 2026 statement, the Federal Open Market Committee (FOMC) noted that “uncertainty about the economic outlook remains elevated” and “the implications of developments in the Middle East for the U.S. economy are uncertain.” The FOMC emphasized that it is “attentive to the risks to both sides of its dual mandate.”

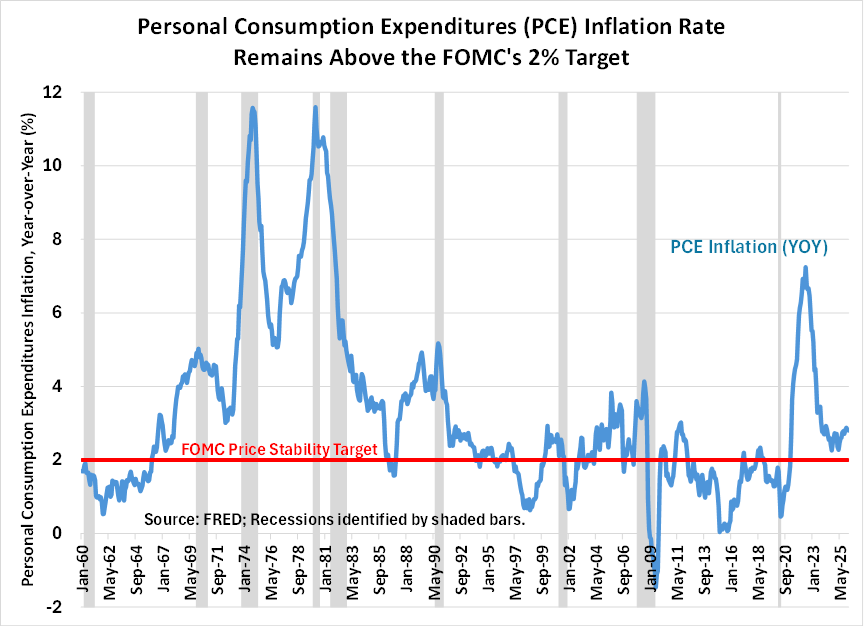

But even before the escalation of conflict in the Middle East, the economic environment was becoming more challenging. Job growth has slowed, partly reflecting reduced immigration and emerging productivity gains from AI adoption. At the same time, inflation has remained above the Fed’s 2% target. As shown in Chart 3, inflation has persisted above target for five years, the longest streak since the metric was officially adopted as a price stability target in 2012. The additional pressures from rising oil prices and potential supply chain disruptions, particularly through the Strait of Hormuz, further complicate the policy outlook.

Community bankers are clearly attuned to these risks. Many respondents pointed to national and global uncertainties—including geopolitical tensions, inflation, labor market dynamics, and rapid technological change—as key concerns. At the same time, a consistent theme has emerged: while uncertainty is elevated at the national level, conditions in many local markets remain comparatively strong.

Several comments from community bank respondents illustrate this contrast:

- “I'm not concerned about local market conditions… I am concerned about the national direction.”

- “Uncertainty continues to play havoc in the markets, but growth in our market still appears strong.”

- “Lots of uncertainty… but loans seem to still be holding up and bank earnings are good right now.”

- “Recent geopolitical events may completely change a number of economic outcomes.”

These perspectives underscore an important distinction. While the national economic outlook remains cloudy, and clarity may take time to emerge, community bankers operate from a different vantage point. Their close relationships with customers and businesses provide real-time insight into local economic conditions, enabling more effective risk management. Many also serve specialized or niche markets, giving them a deeper understanding of sector-specific risks and opportunities that can help mitigate broader economic volatility.

As a result, even as national headlines emphasize uncertainty and downside risks, community bankers often maintain a more grounded view—and at times a more optimistic one—shaped by local realities.

Local Resilience in a Clouded National Outlook

The CBSI suggests that while community bankers are increasingly uncertain about the direction of monetary policy and the national outlook, underlying conditions in many local markets remain stable and, in some cases, strong. The key policy implication is that rising uncertainty at the national level should not be mistaken for broad-based economic weakness.

For policymakers and regulators, this underscores the importance of pairing aggregate data with ground-level intelligence. In an environment shaped by geopolitical shocks and structural shifts, policy that is overly reactive to national volatility runs the risk of tightening or loosening conditions at the wrong time. A measured, data-informed, and locally aware approach will be critical to navigating the current crosscurrents.