Data Corner: PPP Data Highlights Significance of State-Chartered Banks, CSBS Analysis Shows

State-chartered banks were the primary distributor of relief funds to communities, according to a new analysis by CSBS. The analysis matched recently available loan-level Paycheck Protection Program (PPP) data with lender demographic data, providing the first estimate of how different types of lenders originated PPP loans for small businesses around the country.

Specifically, the analysis revealed that, as of July 1, 2021:

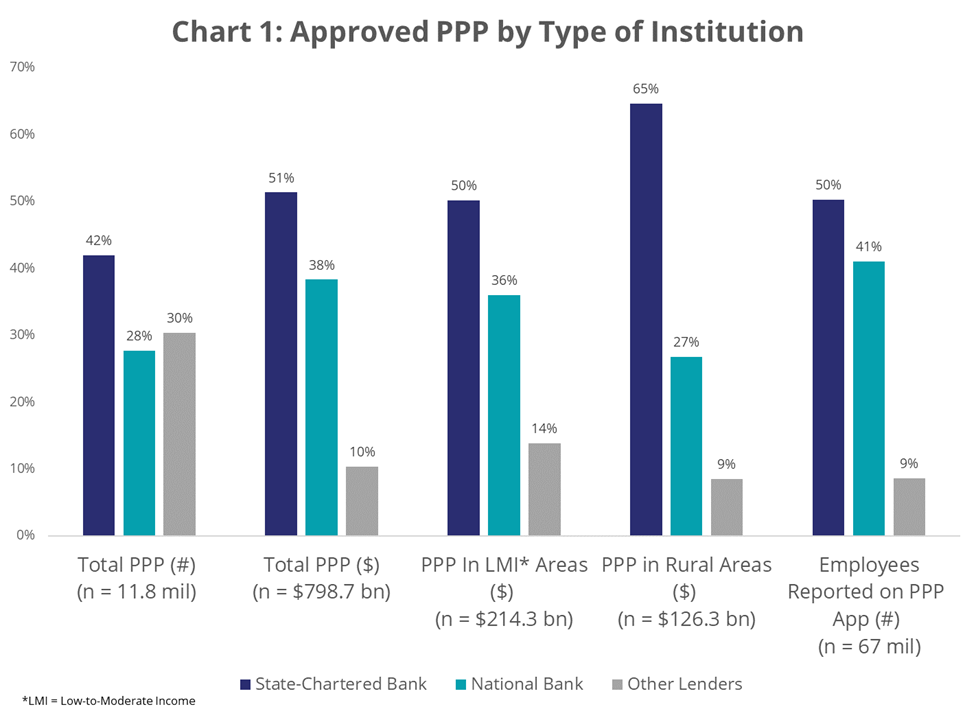

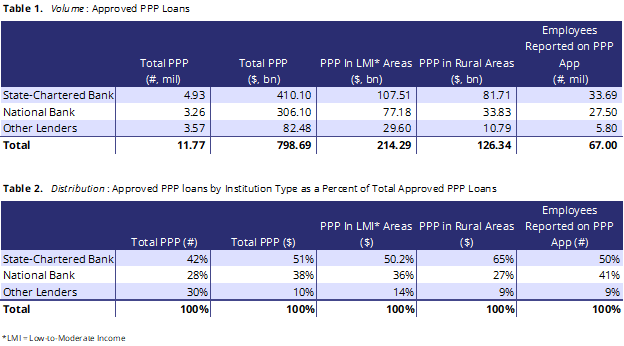

- State-chartered banks provided 51% of all PPP funding by dollar volume. State-chartered banks provided $410.1 billion in total PPP funding, national banks provided $306.1 billion in PPP funding, and other lenders provided $82.5 billion in PPP funding.

- State-chartered banks originated 42% of total PPP loans by number of loans. State chartered banks originated 4.93 million PPP loans, national banks originated 3.26 million loans, and other lenders originated 3.57 million loans.

- State-chartered banks saved more than 50% of the 66+ million jobs the program saved. State-chartered banks saved 33.7 million jobs by connecting small businesses across the country with critical COVID relief in the form of PPP loans. National banks saved 27.5 million jobs, and other lenders saved 8.1 million jobs.

- State-chartered banks were the predominant force in PPP lending to rural areas, providing 65% of all PPP funding by dollar volume to small businesses in rural areas. State-chartered banks provided $81.7 billion in PPP funding in rural areas, national banks provided $33.8 billion in PPP funding in rural areas, and other lenders provided $10.8 billion in PPP funding in rural areas.

- State-chartered banks provided 50% of all PPP funding by dollar volume in low-to-moderate income areas. State-chartered banks provided $107.5 billion in PPP funding in low-to-moderate income (LMI) areas, national banks provided $77.2 billion in PPP funding in LMI areas, and other lenders provided $29.6 billion in funding in LMI areas.

Chart 1 and Table 2 illustrate the distribution of PPP loans, employees reported and dollar volume for state-chartered banks, national banks, and other lenders. Table 1 provides the raw unadjusted counts.

This analysis uses loan-level Paycheck Protection Program (PPP) data provided by the U.S. Small Business Administration (SBA) as of July 1, 2021, and FFIEC bank call report or income and condition data.

Methodology:

Although the PPP data contain the name and state of the originating institution, they do not contain an identifier for the institutions that would make it possible to link this dataset to other bank demographic datasets, making it difficult to understand the characteristics of originating institutions. To overcome this challenge, CSBS used a “fuzzy logic” matching process to identify depository institutions in the data by matching their name, city and state to a panel of data that contains name and state for FDIC-insured depository institutions.

Due to variations in naming (“Sample Bank NA” vs. “Sample Bank NA, d/b/a ThisBank, a Utah Company”) fuzzy logic matching is not a perfect process – but CSBS was able to match about 70% of the 11.7 million PPP loans to a corresponding depository institution. For purposes of this analysis, CSBS refers to remaining 30% of unmatched records as others or other lenders.

The 70% of PPP records, for which CSBS was able to match to a specific depository institution, represented 4,187 banks. Since all banks are required to report PPP loans outstanding in their quarterly call report filings to the FFIEC, CSBS determined that there have been 4,343 banks who have ever reported PPP loans outstanding on the call report. This means that while only 70% of the PPP records were matched with a depository institution, those 70% of matched records account for 96% of the banks that have ever reported PPP loans outstanding (4,187 / 4,343 = 96%).

Furthermore, CSBS estimates that unmatched depositories account for approximately 120,000 PPP loans; therefore only 1% of the 11.8 million loans in the dataset. CSBS believes it has correctly matched all depositories who originated more than 3,000 PPP loans. While it is possible to match this remaining 1%, it would not change any of the findings of this analysis. Since the matching process is imperfect, readers should interpret and use the results with these caveats in mind.

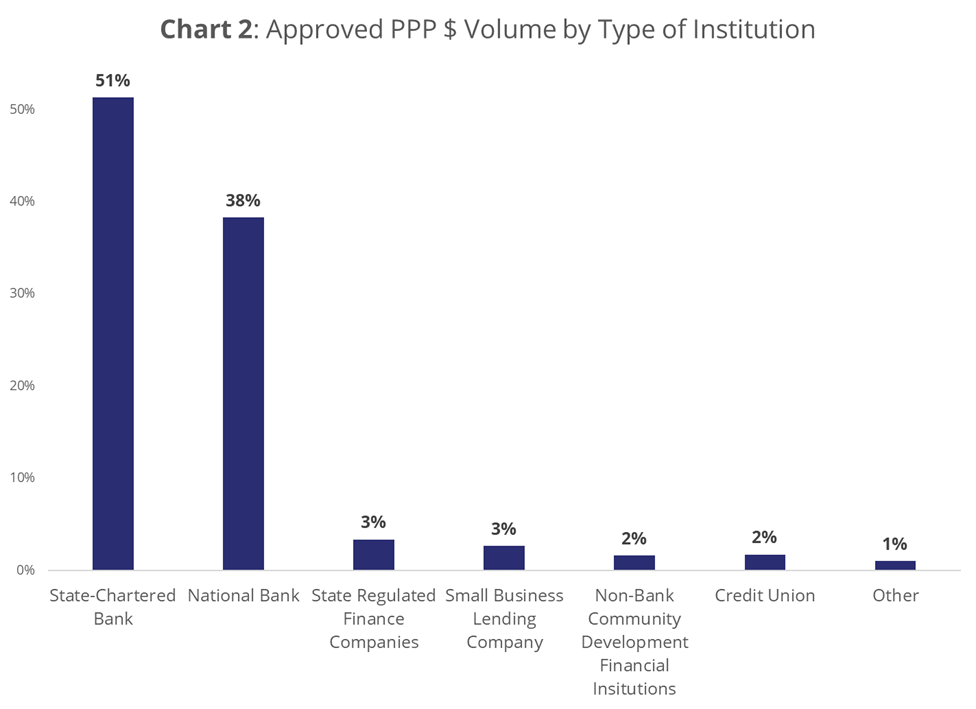

An analysis of the other lender/unmatched/non-bank population breaks down the other lender category into more specific types who provided the following shares of PPP funding by $ volume – illustrated in Chart 2 (categories assigned by SBA):

- 3% of all PPP $ volume was originated by state regulated finance companies.

- 3% of all PPP $ volume was originated by small business lending companies.

- 2% of all PPP $ volume was originated by nonbank community development financial institutions.

- 2% of all PPP $ volume was originated by credit unions.

- 1% of all PPP $ volume was originated by “other” lenders including farm credit administration members, non-profit lenders and certified development companies.

On every application for a PPP loan, the borrower is asked how many employees their small business has. This self-reported “employee count” is included in the loan-level dataset, so when CSBS talks about how many jobs different types of banks saved they are referring to the number of employees reported on each PPP application as reported by the prospective borrower. This does not mean that every employee in a small business was a direct recipient of PPP loan proceeds, since there are restrictions on how funds can be used. CSBS excluded second-draw loans from its tally of employees reported by PPP borrowers to avoid double counting in its jobs saved analysis.

For state-specific data and information, contact [email protected].

Get Updates

Subscribe to CSBS

Stay up to date with the CSBS newsletter