Did Community Banker Sentiment Falter Further After the March 2023 Bank Closures?

By CSBS Chief Economist Thomas F. Siems, Ph.D.

Last month’s high-tech bank runs, liquidity complications and subsequent closure of three high-profile banks surprised many bankers and investors. While the FDIC and the Federal Reserve acted quickly to maintain confidence by providing a higher backstop for depositors and creating greater lending capacity for all financial institutions through the Fed’s Bank Term Funding Program, community banker sentiment fell further from an already record-low. Following the March 9 events, community banker sentiment was driven lower mainly from expectations that the industry’s regulatory environment could become more burdensome and that economic and financial conditions could worsen.

The first quarter 2023 Community Bank Sentiment Index (CBSI), released on April 4, showed that community bankers are more pessimistic now than at any time since the survey’s inception in 2019. The overall index was 83, where 100 is considered the neutral level, values above 100 indicate expansion and those below 100 signal contraction. The quarterly CBSI averaged 122 in 2019, dropped significantly to 94 in 2020 with the pandemic/economic lockdowns, rose to 107 in 2021 as the economy began recovering and then fell again to 89 in 2022 as high inflation and weak economic growth persisted.

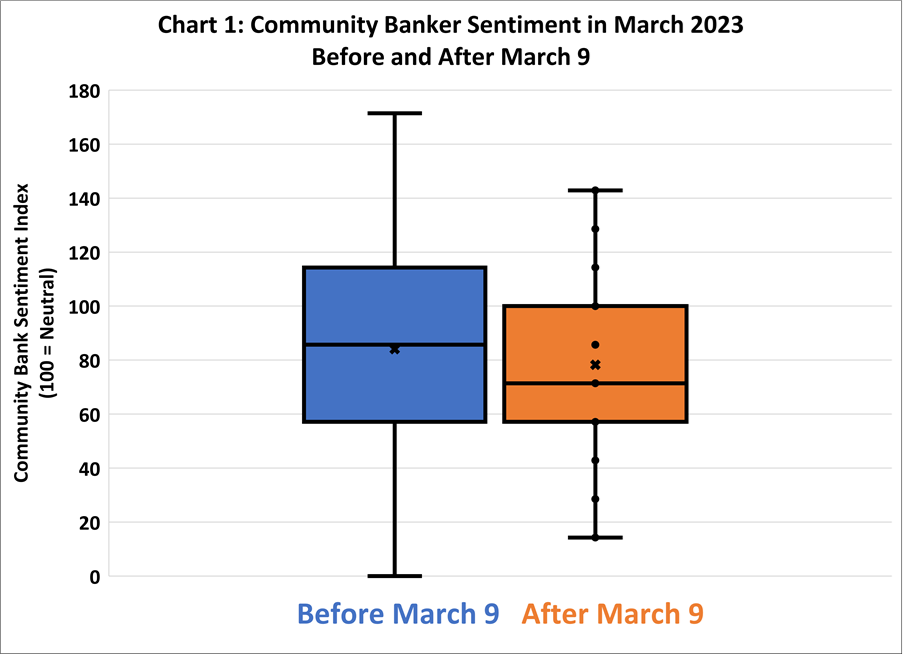

Because the CBSI survey was open to community bankers throughout March, we can investigate the responses before and after the banking problems that were exposed on March 9 to uncover any differences in sentiment.

For the composite CBSI, Chart 1 shows average community banker sentiment (displayed with an “x”) dropped from 84 before March 9 to 78 for those bankers who completed the survey during the final three weeks of March. The boxes in the chart highlight the distribution of data in each group by displaying the interquartile range of responses (first quartile to third quartile; the center line in the box is the median). The whiskers on each chart show the overall range of values for each group. It is worth noting that only 22% of the monthly responses came in after March 9, which is why the composite CBSI for the monthly survey (83) dropped by only one point from the average reading before the banking issues emerged.

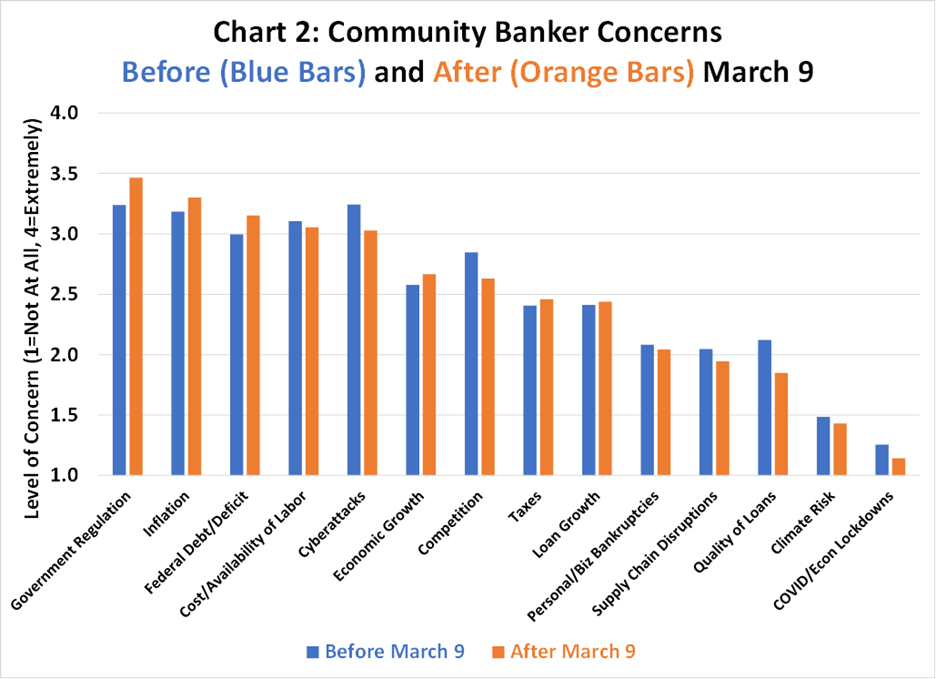

For the seven components that comprise the CBSI, the indicator that fell furthest was also the one already at the lowest level. The “regulatory burden” component, historically pulling the overall index down the most, dropped from 26 before the mid-March banking problems to 10 afterward. Moreover, in a special question, “government regulation” rose to the top of the list of community banker concerns, surpassing “inflation” as the top concern for the first time since the end of 2021.

And, as shown in Chart 2, community banker concerns of heavier “government regulation” increased significantly in the days and weeks following the March 9 events. Before the bank closures, government regulation was tied with cyberattacks as the top concern. After the bank closures, concern over a heavier regulatory environment showed a statistically significant increase from 3.24 (on a 4.0 scale) to 3.47, the most significant increase among the fourteen worries on the list.

It is also interesting to note the three other “concerns” that increased by 0.09 or more: federal debt/deficit (up 0.16), inflation (up 0.12), and economic growth (up 0.09). The liquidity struggles influenced by the Fed’s rapid rate increases since March 2022 and the Fed’s apparent policy dilemma of fighting inflation on the one hand, and maintaining financial stability on the other hand, have heightened community banker worries of slower economic growth, higher inflation, and larger federal deficits.

In summary, community banker sentiment was in the doldrums before the liquidity problems at certain banks in mid-March 2023 were obvious but slipped further in the weeks following the closures of these institutions. Driving community banker sentiment lower are concerns that government regulation could become more burdensome, apparently through either new legislation designed to prevent similar liquidity problems in the future or more forceful supervisory actions as banks continue to adjust to the significantly higher interest rate environment. Furthermore, after the bank closures, community bankers appear more concerned about weaker economic growth, higher inflation and larger federal deficits as policymakers manage considerable economic and financial risks.